Recording & Acknowledging In-Kind Gifts: Nonprofit Tax Tips

Recording and acknowledging in-kind gifts is a specialized accounting process for nonprofits and other charitable organizations to track non-cash contributions, such as donated goods or professional services. Per the Financial Accounting Standards Board, these donations must be documented as “Contributed Nonfinancial Assets,” requiring nonprofits to reconcile impact value with tax compliance to ensure transparency and maintain donor trust.

According to recent research, U.S. donors (including individuals, businesses, and government agencies) contribute an estimated $58 billion worth of in-kind gifts to nonprofits each year. From a local law firm providing pro bono counsel to a tech giant donating high-end servers, non-cash contributions allow organizations to bridge the gap between limited budgets and ambitious goals.

In this guide, we’ll explore helpful tips for effectively recording, valuing, and acknowledging in-kind gifts:

- Defining the In-Kind Landscape: More Than Just “Old Stuff”

- Recording an In-Kind Gift According to FASB & GAAP Standards

- Valuing an In-Kind Donation: Determining the Fair Market Value

- Acknowledging In-Kind Gifts: Maintaining IRS Compliance

- Company-Specific Tips for Managing the Corporate Partnership

- Bonus: Common In-Kind Donation Pitfalls to Avoid

In-kind donations are often a double-edged sword. While they provide immense value to nonprofits, they also present a unique set of accounting and compliance hurdles. In the eyes of the law, a $5,000 check is straightforward; $5,000 worth of “lightly used office furniture” or “marketing consulting hours” is anything but.

Let’s dive in to discover how your team can manage these donations effectively.

Defining the In-Kind Landscape: More Than Just “Old Stuff”

Before we tackle the tax forms, it’s essential that you first understand what constitutes an in-kind gift.

Tangible Goods (Products)

As the most common form of corporate in-kind giving, tangible goods can include:

- Surplus Inventory: A retailer gifting last season’s coats to a homeless shelter, or a bakery contributing unsold food and beverage items to local food banks

- Equipment: A company donating its previous technology to a local school after refreshing its internal hardware systems

- Supplies: A company contributing paper, cleaning supplies, or event materials (e.g., decorations or catering)

Professional Services (Pro Bono)

Services are one of the most valuable and most frequently mismanaged types of in-kind gifts. For a service to be considered recordable on your financial statements, it must generally require specialized skills, be provided by someone possessing those skills, and be a service your nonprofit would otherwise have to pay for.

This could include:

- Legal & Accounting: Audit services or contract reviews

- Marketing & Creative: Graphic design, website development, or search engine optimization efforts

- Trade Services: Electrical work, plumbing, or construction

Intangible Assets and Facilities

This final, often-overlooked category includes the use of assets. Here are a few examples:

- Rent-Free Space: A business allowing a nonprofit to use a storefront or office suite at no cost

- Advertising Credits: Donated airtime or digital ad spend (like the Google Ad Grant)

Focusing on in-kind donations from companies isn’t just about saving money; it’s about resource amplification. When a corporation gives you $10,000 in cash, it gives you $10,000 in buying power. However, when they give you $10,000 worth of their own product, the “cost” to them might only be $4,000 (their wholesale cost), but the “value” to you is the full $10,000. This creates a win-win: the company makes a significant impact at a lower internal cost, and your nonprofit receives high-quality resources.

Furthermore, in-kind gifts often act as a “gateway” to larger corporate sponsorships. A company that begins by donating printing services for your annual gala is more likely to become a cash sponsor once they see the professionalism and impact of your work.

Recording an In-Kind Gift According to FASB Standards

As of 2020, nonprofits must adhere to specific reporting criteria set forth in the Financial Accounting Standards Board’s FASB ASU 2020-07. This standard was designed to increase transparency regarding how nonprofits use and value nonfinancial assets.

In other words, organizations can no longer hide in-kind gifts in their general contribution revenue. Now, on their Statement of Activities, they must report “Contributed Nonfinancial Assets” as a separate line item from cash contributions.

Additionally, organizations are now required to break down in-kind gifts by category (e.g., “Food Supplies,” “Legal Services,” “Technology Equipment”) within the notes of their financial statements. For each category, it’s important to disclose:

- Usage vs. Monetization: Did you use the items in your programs, or did you sell them (like at a silent auction)?

- The Valuation Method: How did you determine the price? (e.g., wholesale market price or local retail rates).

- Donor Restrictions: Were there any strings attached? (e.g., “this software can only be used for our youth program”).

Wondering how and where volunteer hours come into play? This is a common point of confusion for many organizations. If a volunteer helps you paint your office, you generally do not record that as in-kind revenue. However, if a professional painting company donates its time to paint your office, you do record it.

Here’s a helpful rule: If you would have otherwise had to pay a professional to do it, and a professional did it for free, record it.

Valuing an In-Kind Donation: Determining the Fair Market Value

Perhaps the most stressful part of in-kind gift management is the valuation process. Who decides what a 5-year-old van or a custom-coded database is worth? That’s where the idea of fair market value (or FMV) is introduced.

In the context of in-kind donations, Fair Market Value is the price that would typically be received for the sale of an asset in an orderly transaction between market participants at the measurement date. Essentially, that means it’s the “sticker price” the item would fetch on the open market if you were a regular buyer and seller.

As a nonprofit, here’s how you can determine a gift’s fair market value for your own internal records:

- For Goods: Use the “comparable sales” method. What would it cost to buy that item in its current condition on the open market? Websites like eBay or specialized refurbished equipment retailers can be great assets for this.

- For Services: Ask the professional for their standard hourly rate. If a lawyer who usually charges $400/hour gives you 10 hours of work, your internal record should show a $4,000 in-kind gift.

- For Space: Use the local price per square foot for similar commercial properties in your area.

However, IRS regulations are very clear: It’s the donor’s responsibility, not the nonprofit’s, to determine the value of the gift for their own tax deduction. Your job is to provide a “good faith estimate” for your internal accounting, but you should never provide a valuation on the official receipt you send to the donor.

Acknowledging In-Kind Gifts: Maintaining IRS Compliance

When it comes to strengthening supporter relationships, whether corporate or individual, acknowledging in-kind gifts can go a long way.

To ensure your donors (especially businesses) can actually claim their tax deduction, your acknowledgment letter must be precise. For any gift valued at $250 or more, the donor must have a “contemporaneous written acknowledgment.”

Here’s what the IRS states the letter MUST include:

- The name of your Organization and your EIN (or Tax ID number)

- A description of the gift: Be specific. Instead of “Computer equipment,” write “Five 2023 MacBook Pro laptops.”

- The “Goods and Services” statement: You must state whether or not the organization provided any goods or services in return for the donation. Example: “No goods or services were provided in exchange for this contribution.”

- Quid Pro Quo disclosures: If you did provide something (e.g., a donor gave you a $500 printer and you gave them two tickets to a $50 dinner in return), you must provide a good-faith estimate of the value of that dinner and subtract it from their potential deduction.

Keep in mind that you should not provide a dollar amount for donations of goods or other physical items. The donor fills that in on their own tax forms.

The 2026 Threshold Update

For the 2026 tax year, the IRS has adjusted its “low-cost article” thresholds. If you give a donor a token item, such as a coffee mug with your logo, in exchange for their gift, it is considered insubstantial value if its cost is no more than 2% of the donation or $139 (whichever is less). If it falls under this threshold, you don’t need to deduct it from the value of the donor’s gift.

Company-Specific Tips for Managing the Corporate Partnership

For-profit businesses are often the leaders in in-kind donations. Companies contribute more than $4 billion to nonprofit causes in the form of goods and services each year.

When dealing with corporate donors, the in-kind donation recording process is often part of a larger relationship-management strategy. Here are some helpful tips to boost corporate giving through non-financial donations.

The Impact Report

In addition to the standard tax receipt, it’s a good idea to send corporate donors a dedicated Impact Report. If a business donated 500 cases of water for your marathon, share a photo of the water station with a personalized note saying: “Your donation saved us $2,500 in event costs, which we redirected to provide 100 additional health screenings for our community.”

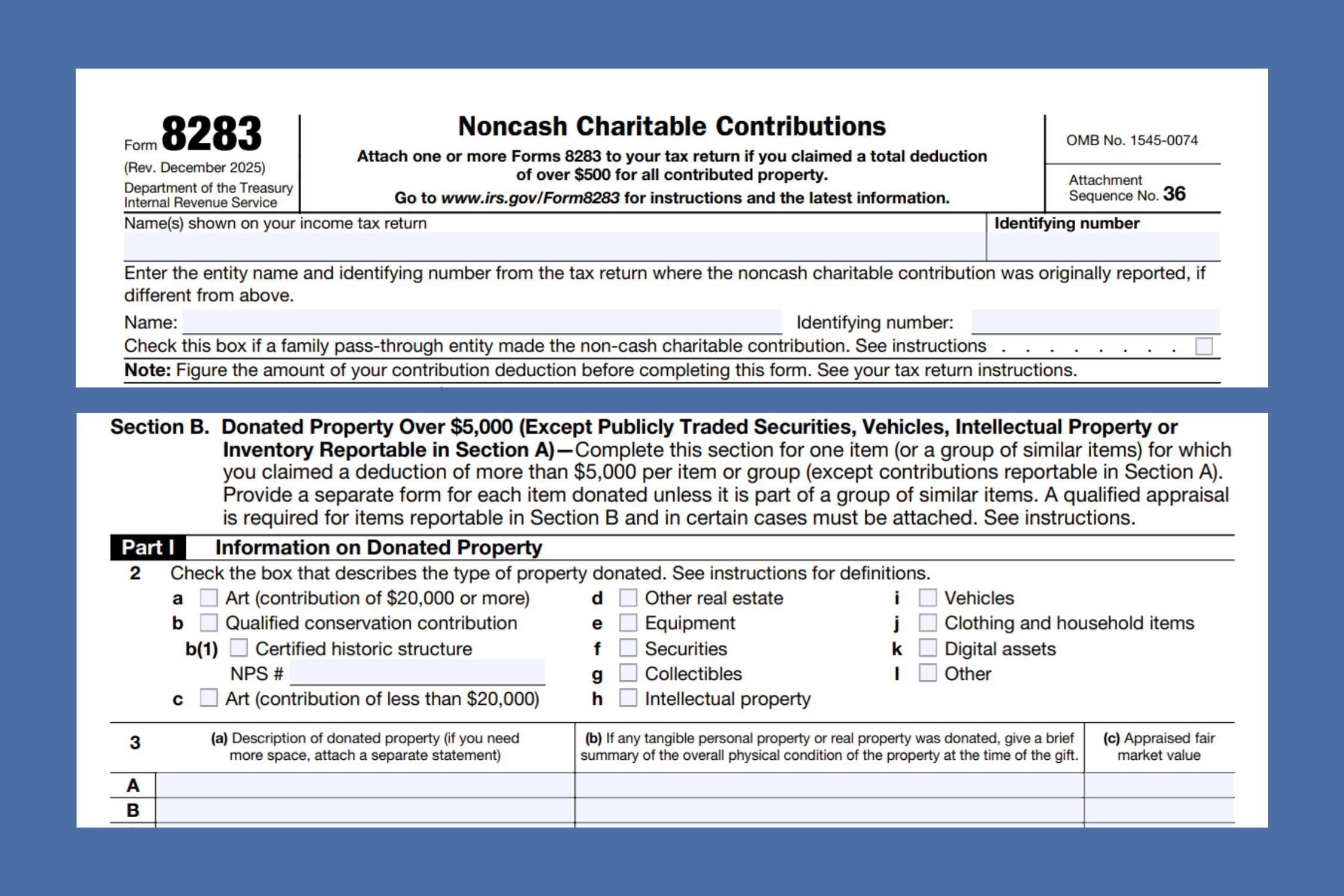

Form 8283 and Reaching the $5,000 Mark

If a company contributes a non-cash item valued at over $5,000, they will likely ask you to sign IRS Form 8283.

By signing this form, you acknowledge that you received the property. You are not, however, vouching for the value the donor has claimed.

For items worth more than $5,000, the donor must obtain a qualified appraisal to deduct the contribution from their taxes. However, this is their expense, not yours.

Public Recognition as Partner Marketing

Corporate donors often value the “halo effect” that comes with charitable giving. Play it up by offering to feature their logo on your website, social media, or event signage, specifically as an In-Kind Partner. Highlighting their brand in connection to a successful project, such as “Software provided by [Company Name],” provides them with valuable marketing exposure and social proof of their community involvement.

This recognition often paves the way for future cash grants or other sponsorships, as the company already feels invested in your success.

Bonus: Common In-Kind Donation Pitfalls to Avoid

Recording, valuing, and acknowledging in-kind gifts is often more complex than handling cash alone. While these donations are vital, they can create administrative burdens or legal risks if not managed properly. Here is a comprehensive analysis of common mistakes nonprofits make and how your organization can navigate them.

Pitfall A: The “Free” Trap (Accepting Everything)

The most common mistake stems from the scarcity mindset. This is the belief that a nonprofit should never turn down a donation. However, accepting items that aren’t aligned with your mission or operational needs can quickly turn into a financial drain.

For example, a gift of 50 obsolete, broken printers isn’t a contribution; it’s a disposal liability. You will spend staff time moving them, valuable square footage storing them, and eventually, budget dollars to recycle them responsibly.

How to Overcome This Pitfall:

- Establish a Gift Acceptance Policy: Create a formal gift acceptance policy that explicitly lists “Accepted” vs. “Declined” items. For example, you might accept vehicles only if they are in working order or technology only if it is less than three years old.

- The “Cost of Gift” Assessment: Train your intake team to ask: “Will this cost us more to manage than it’s worth?” If a donation requires specialized climate control, insurance, or significant repair, it may be better to politely decline and suggest a partner organization that is better equipped to handle it.

Pitfall B: Mischaracterizing “Partial” Gifts and Discounts

Nonprofits often struggle with recording “special deals.” If a local venue gives you a 50% discount on a room rental, you might be tempted to record the discount as an in-kind gift. However, a donor generally cannot take a tax deduction for giving a nonprofit the right to use property (like a rent-free office) while they still own it.

How to Overcome This Pitfall:

- Distinguish Accounting vs. Tax: Understand that what you record on your financial statements (GAAP) may differ from what the donor can deduct (IRS). You should record the value of the space used for financial transparency, but your acknowledgment letter should never promise a tax deduction for partial interest or time.

- The “Consult Your Advisor” Clause: Always include a standard disclaimer in your receipts: “Our organization has not provided any goods or services in exchange for this contribution. Please consult your tax advisor regarding the deductibility of this gift.” This protects your relationship by placing the burden of tax-law compliance on the donor’s professional counsel.

Pitfall C: Forgetting the Audit Trail (The Documentation Gap)

In-kind gifts are often a high-scrutiny area during audits because their value is subjective. If an auditor sees a $10,000 entry for “Donated Software” but you have no documentation to prove how you arrived at that number, they may flag it as a reporting error. Without a paper trail, you cannot prove that the transaction was orderly or that the value reflects the principal market.

To overcome this pitfall, create a standardized digital folder for every significant in-kind contribution that contains:

- Proof of Intent: The original email or letter from the donor offering the gift.

- Valuation Rationale: A PDF or screenshot of the “Market Approach” used (e.g., a printout of the retail price from a reputable vendor on the date received).

- Receipt of Goods: Internal confirmation (like a warehouse sign-off) that the items were actually received and in the condition described.

- Copy of Acknowledgment: The final letter sent to the donor, which should describe the goods but not assign them a dollar value.

If you have all of the above items on hand, you should pass your audit with flying colors!

Conclusion

In-kind gifts are a testament to the community’s belief in your mission. When a company chooses to share its products or expertise with you, it’s essentially offering a piece of its identity to help fuel your cause. By mastering the “boring” parts (the recording, the valuation, and the IRS-compliant acknowledgment), you protect your nonprofit’s status and build a foundation of trust with your most valuable partners.

Properly handled, an in-kind gift isn’t just a line item on a spreadsheet; it’s a catalyst for growth that can take your impact to the next level.

Disclaimer: This post is for informational purposes only and does not constitute legal or tax advice. Tax laws are subject to change, so we always recommend consulting with a qualified CPA or tax professional regarding your nonprofit’s specific situation.